How to Help Your Kids Without Killing Their Ambition: The 20/60/20 Rule

There's a specific kind of internal friction that comes with success: the desire to help your children financially, balanced against the fear of what that money might do to their ambition.

You've worked hard to build assets so your children don't have to struggle, yet privately, you might be terrified that a large gift—like a house deposit—might rob them of the drive to build something of their own.

Without a clear strategy, "too much" becomes a genuine risk factor.

Giving money away without a plan can inadvertently compromise your own retirement lifestyle or create a dependency you never intended.

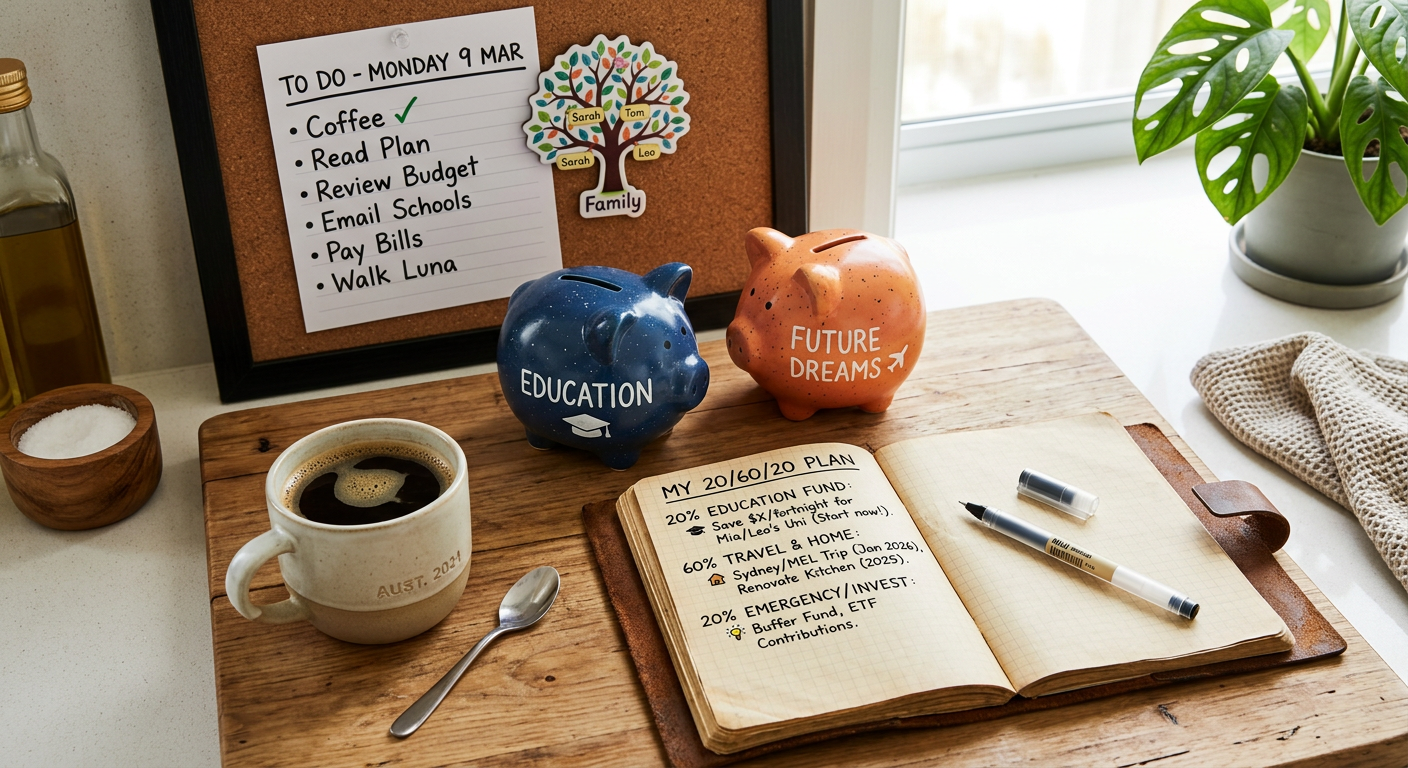

The 20/60/20 Approach to Intergenerational Wealth

To move past the guilt and uncertainty, you need a way to align your cashflow with your family values.

This three-part funding split shifts the focus from a "handout" to a "legacy," ensuring you protect their future while respecting their independence.

1. Allocate 20% to 'Launch' Costs

This portion is for specific, immediate hurdles that provide a clean start.

Think of it as removing the barriers to entry rather than providing a free ride.

Examples include education costs or specific contributions toward a wedding.

By covering these defined events, you give them a leg up without removing the daily necessity for them to earn and manage their own income.

2. Direct 60% into 'Productive Protection'

The majority of your support should be focused on long-term growth rather than immediate liquidity.

This involves investing in structures—such as an ethical investment portfolio or superannuation—where the capital grows for their future.

Because this money isn't accessible for daily spending, it builds a foundation for their mid-life and retirement years while they remain responsible for their current lifestyle.

3. Reserve 20% for the 'Safety Net'

True financial protection means ensuring that if life takes an unexpected turn, your children are protected by professional structures rather than your own retirement savings.

Use this final portion to fund life insurance and disability cover. This prevents your personal wealth from becoming a default emergency fund, preserving your own financial independence and your children's long-term security simultaneously.

The Framework in Action

Imagine a couple wanting to provide $100,000 to their adult child.

Instead of a lump sum house deposit that covers the entire entry cost, they might allocate $20,000 to clear remaining HELP debt (Launch), $60,000 into a managed ethical investment trust or super contribution (Productive Protection), and use the remaining $20,000 to fund high-quality income protection and life insurance premiums for several years (Safety Net).

The result?

The child still has to save for their own home deposit (maintaining their "drive"), but their long-term wealth is secured, and parents' retirement savings are untouched by future crises.

Start the Conversation

The first step in applying this is to assess your current intentions.

Before making that first funds transfer, figure out where your planned gift fits in each of these three funding buckets. Does it skew too heavily toward 'Launch'? If so, you may be creating the very dependency you fear.

If you would like to discuss how to structure your support for the next generation without compromising your own retirement, we can help.

To learn more about aligning your wealth with your principles, you can also Download your free Guide to Ethical Investing or listen to the Get Ethical podcast.